What should I do when involved in an accident?

Auto Accident Claim Guide

- Take a photo of the other party’s vehicle, license plate, and position right after the accident.

- Exchange insurance information. Take a photo of the involved parties' driver's license and insurance Card.

- Ask for the witness's name and phone number if you can.

- Call the police if the other party is not cooperating or if you are injured.

- File a claim with the insurance company and keep the claim number.

- Respond to the claim handler's phone call and letter promptly.

- Find a repair shop of your choice.

- If you have a rental car, exam the rental car before and after use.

- If your own insurance pays for the repair first, you need to pay your deductible. If the other party is at fault and his or her insurance pays for the repair, no deductible applies.

- If total loss, give the key and title to the insurance company.

What is the difference between full coverage and liability coverage?

What is the difference between full coverage and liability coverage?Auto insurance has many different descriptions and coverage, and it is easy to get confused between these. Two main categories of car insurance are liability coverage auto insurance and full coverage car insurance, and the difference between these two can be wide. Vehicle insurance is required in every state in America, and the coverage amount that each state demands will vary from one state to the next, but all states require a minimum liability coverage amount.

Liability car insurance is coverage that occurs when there is an injury or damage to people and property, excluding your vehicle and passengers in the vehicle. There are three sections to liability automobile insurance, the coverage limit per accident for bodily injury per person, the coverage limit maximum for all injuries sustained by all people per accident, and the maximum limit for property damage coverage per accident. It may be wise to purchase more than the required minimum limits of liability vehicle insurance required by your state, to ensure that you have adequate coverage and do not end up with big bills after an accident in addition to insurance coverage.

Full coverage auto insurance includes liability coverage and also includes collision coverage and comprehensive coverage. It is possible to purchase liability and comprehensive coverage without including collision coverage, but if you opt for collision coverage you must include liability and comprehensive. Comprehensive car insurance covers things besides collisions that can cause damage to your vehicle, such as weather related events like tree or hail damage, fires, theft, and even hitting an animal in the road, although most consumers would consider the last one a collision event.

Comprehensive vehicle insurance protects you against any damage to your car that is generally not your doing or fault. Many people do not owe a debt on their vehicle, so they do not get collision or comprehensive car insurance, and this can sometimes be a big mistake. There are several different things to consider before deciding to forgo these auto insurance options, or you could end up regretting your decision. Consider the blue book value of your vehicle, and the maximum you will get from the other drivers car insurance company under no fault or other liability only insurance laws. If your vehicle is fairly new with a good value, then full coverage is a good idea so that you can replace the vehicle in the event it is totaled. Otherwise you may end up unable to afford a replacement vehicle of the same condition or quality, and end up driving junk instead because of no comprehensive or collision auto insurance.

Collision coverage can be added with comprehensive coverage, and if you still owe a balance on financing for the vehicle, most finance companies require collision auto insurance coverage as mandatory. This protects the finance company if there is an accident and your vehicle is totaled, with the car loan being paid off by the insurance payment. It is possible to get full coverage cheap auto insurance if you know about free online automobile insurance quotes. These quotes can help you compare insurance rates and coverage so that you can find the vehicle insurance policy you need, without having to pay more for it.

Source: http://www.2insure4less.com/auto-insurance-quotes/auto-insurance-guide/what-is-the-difference-between-full-coverage-and-liability-coverage

Copyright @ 2016 Grace Insurance Services. All rights reserved. Terms of service privacy.

Liability car insurance is coverage that occurs when there is an injury or damage to people and property, excluding your vehicle and passengers in the vehicle. There are three sections to liability automobile insurance, the coverage limit per accident for bodily injury per person, the coverage limit maximum for all injuries sustained by all people per accident, and the maximum limit for property damage coverage per accident. It may be wise to purchase more than the required minimum limits of liability vehicle insurance required by your state, to ensure that you have adequate coverage and do not end up with big bills after an accident in addition to insurance coverage.

Full coverage auto insurance includes liability coverage and also includes collision coverage and comprehensive coverage. It is possible to purchase liability and comprehensive coverage without including collision coverage, but if you opt for collision coverage you must include liability and comprehensive. Comprehensive car insurance covers things besides collisions that can cause damage to your vehicle, such as weather related events like tree or hail damage, fires, theft, and even hitting an animal in the road, although most consumers would consider the last one a collision event.

Comprehensive vehicle insurance protects you against any damage to your car that is generally not your doing or fault. Many people do not owe a debt on their vehicle, so they do not get collision or comprehensive car insurance, and this can sometimes be a big mistake. There are several different things to consider before deciding to forgo these auto insurance options, or you could end up regretting your decision. Consider the blue book value of your vehicle, and the maximum you will get from the other drivers car insurance company under no fault or other liability only insurance laws. If your vehicle is fairly new with a good value, then full coverage is a good idea so that you can replace the vehicle in the event it is totaled. Otherwise you may end up unable to afford a replacement vehicle of the same condition or quality, and end up driving junk instead because of no comprehensive or collision auto insurance.

Collision coverage can be added with comprehensive coverage, and if you still owe a balance on financing for the vehicle, most finance companies require collision auto insurance coverage as mandatory. This protects the finance company if there is an accident and your vehicle is totaled, with the car loan being paid off by the insurance payment. It is possible to get full coverage cheap auto insurance if you know about free online automobile insurance quotes. These quotes can help you compare insurance rates and coverage so that you can find the vehicle insurance policy you need, without having to pay more for it.

Source: http://www.2insure4less.com/auto-insurance-quotes/auto-insurance-guide/what-is-the-difference-between-full-coverage-and-liability-coverage

Copyright @ 2016 Grace Insurance Services. All rights reserved. Terms of service privacy.

How can I receive rates for other car insurance company?

To receive rates for other leading auto insurers in your state, you must get a car insurance quote first. Once you receive your quote, you can answer a few more questions to compare our rate with rates from other leading car insurance companies.

liability coverage and car value?

1. State Minimums

Liability insurance is typically quoted in three categories, including personal injury to a single person, personal injury for all persons and property damage. Each category is usually quoted in thousands and divided by hash marks (/). Minimum levels of liability insurance vary from state to state and range from 10/20/10 in Florida to 50/100/55 in Wisconsin. New Hampshire is only state in the union that does not require automobile operators to maintain a minimum level of auto liability insurance, as of September 2010. However, New Hampshire does require a minimum level of uninsured motorist coverage.

2. Bodily Injury

The bodily injury component of car insurance is quoted in two sections, including bodily injuries sustained by one person and bodily injuries sustained by all persons involved in an at-fault accident. It is important to understand that the driver of the vehicle in an at-fault accident is not covered by her liability insurance policy. Bodily injury liability insurance covers against financial loss for medical expenses, funeral costs and legal fees. The North America Military Financial Education Center (NAMFEC) at the University of Maryland recommends drivers carry at least $100,000 per person and $300,000 per incident in bodily injury liability insurance.

3. Property Damage

The property damage component of car insurance covers against financial loss if the insured vehicle causes damage to another person's property. The damaged property may include another vehicle, a home, a mailbox, a fence or personal property inside the damaged vehicle. Property damage liability insurance also covers legal expenses in the event of a lawsuit. Property damage liability insurance does not cover financial loss resulting from damage to the insured's property. The NAMFEC recommends maintaining a minimum of $100,000 in property damage liability coverage.

4. Uninsured Motorist Insurance

Liability insurance protects an at-fault driver against financial loss associated with property damage or bodily injury to others. It does not protect the at-fault driver against personal injury to himself or property damage sustained by the vehicle he was driving. Liability insurance does not protect anyone in the event of an accident caused by another party. Edmunds estimates more than 16 percent of drivers are either uninsured or under insured. The NAMFEC recommends maintaining a minimum of $100,000 per person and $300,000 per accident of uninsured/under insured motorist insurance.

Source:http://www.ehow.com/info_7747241_recommended-amount-car-liability-insurance.html

Liability insurance is typically quoted in three categories, including personal injury to a single person, personal injury for all persons and property damage. Each category is usually quoted in thousands and divided by hash marks (/). Minimum levels of liability insurance vary from state to state and range from 10/20/10 in Florida to 50/100/55 in Wisconsin. New Hampshire is only state in the union that does not require automobile operators to maintain a minimum level of auto liability insurance, as of September 2010. However, New Hampshire does require a minimum level of uninsured motorist coverage.

2. Bodily Injury

The bodily injury component of car insurance is quoted in two sections, including bodily injuries sustained by one person and bodily injuries sustained by all persons involved in an at-fault accident. It is important to understand that the driver of the vehicle in an at-fault accident is not covered by her liability insurance policy. Bodily injury liability insurance covers against financial loss for medical expenses, funeral costs and legal fees. The North America Military Financial Education Center (NAMFEC) at the University of Maryland recommends drivers carry at least $100,000 per person and $300,000 per incident in bodily injury liability insurance.

3. Property Damage

The property damage component of car insurance covers against financial loss if the insured vehicle causes damage to another person's property. The damaged property may include another vehicle, a home, a mailbox, a fence or personal property inside the damaged vehicle. Property damage liability insurance also covers legal expenses in the event of a lawsuit. Property damage liability insurance does not cover financial loss resulting from damage to the insured's property. The NAMFEC recommends maintaining a minimum of $100,000 in property damage liability coverage.

4. Uninsured Motorist Insurance

Liability insurance protects an at-fault driver against financial loss associated with property damage or bodily injury to others. It does not protect the at-fault driver against personal injury to himself or property damage sustained by the vehicle he was driving. Liability insurance does not protect anyone in the event of an accident caused by another party. Edmunds estimates more than 16 percent of drivers are either uninsured or under insured. The NAMFEC recommends maintaining a minimum of $100,000 per person and $300,000 per accident of uninsured/under insured motorist insurance.

Source:http://www.ehow.com/info_7747241_recommended-amount-car-liability-insurance.html

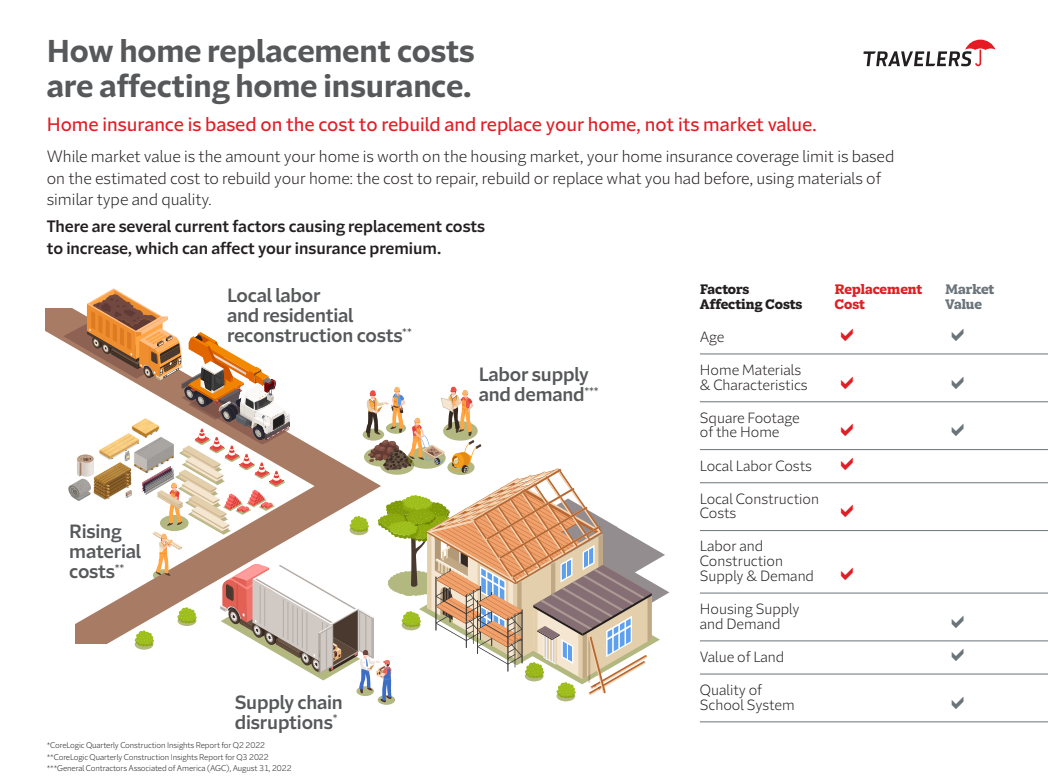

HOW HOME REPLACEMENT COSTS ARE AFFECTING HOME INSURANCE.

What is replacement cost?

Replacement cost is the amount it would take to repair, replace, or rebuild your home at current prices of construction materials and labor.

When you insure your home for its estimated replacement cost, you help to ensure you have the coverage you need to repair or rebuild if it is damaged by a covered loss.

What is market value?

Market value is the amount your home is worth on the housing market.

Why is the coverage limit of my home higher or lower than the home’s market value?

Your home insurance amounts are based on its estimated replacement cost, or the cost to rebuild, and not the amount it would sell for on the housing market.

Why does Travelers review coverage limits annually and make adjustments to coverage limits?

Travelers wants to help you rebuild and replace what you had before. Coverage limits are reviewed annually and estimated using a number of factors. Depending on market conditions and any upgrades you may have made, coverage amounts may need to be adjusted.

Why are many policyholders seeing increases in their coverage limits in 2022?

Coverage limits need to keep up with rising inflation. This is an industry-wide issue. As mentioned above, many factors are considered when estimating your coverage. One of these factors is reconstruction costs. Reconstruction costs have risen steadily since our last assessment.

Why Travelers?

We think you will find that Travelers continues to compare favorably with other carriers, offering outstanding coverage and claim service.

Replacement cost is the amount it would take to repair, replace, or rebuild your home at current prices of construction materials and labor.

When you insure your home for its estimated replacement cost, you help to ensure you have the coverage you need to repair or rebuild if it is damaged by a covered loss.

What is market value?

Market value is the amount your home is worth on the housing market.

Why is the coverage limit of my home higher or lower than the home’s market value?

Your home insurance amounts are based on its estimated replacement cost, or the cost to rebuild, and not the amount it would sell for on the housing market.

Why does Travelers review coverage limits annually and make adjustments to coverage limits?

Travelers wants to help you rebuild and replace what you had before. Coverage limits are reviewed annually and estimated using a number of factors. Depending on market conditions and any upgrades you may have made, coverage amounts may need to be adjusted.

Why are many policyholders seeing increases in their coverage limits in 2022?

Coverage limits need to keep up with rising inflation. This is an industry-wide issue. As mentioned above, many factors are considered when estimating your coverage. One of these factors is reconstruction costs. Reconstruction costs have risen steadily since our last assessment.

Why Travelers?

We think you will find that Travelers continues to compare favorably with other carriers, offering outstanding coverage and claim service.

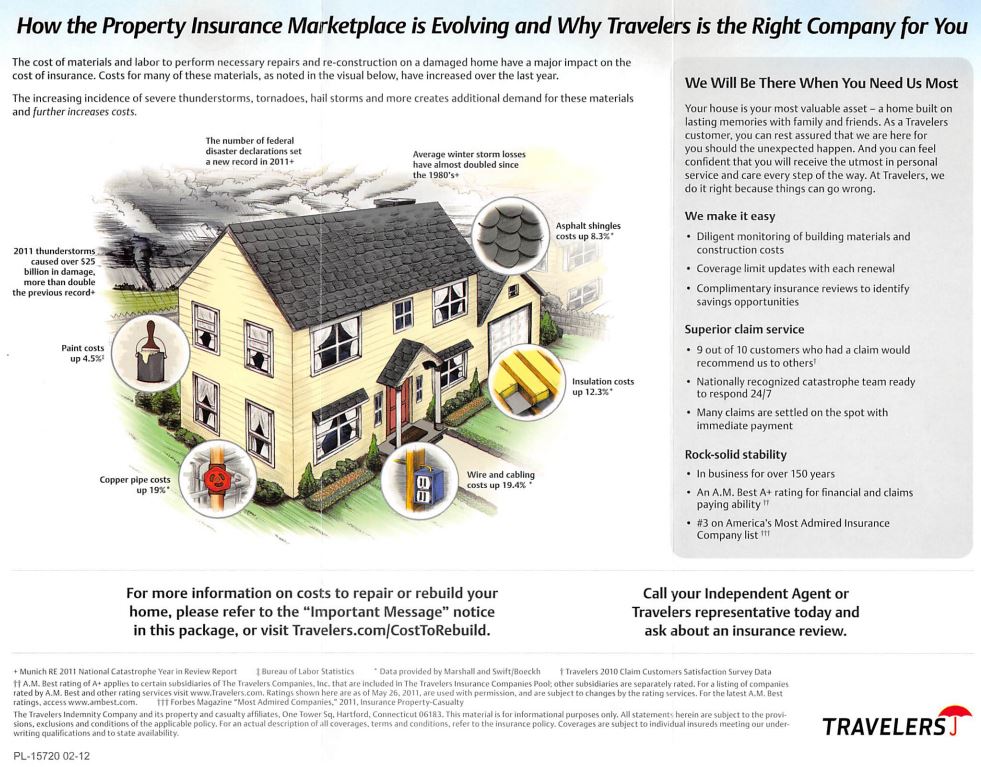

HOW IS THE PROPERTY INSURANCE MARKETPLACE EVOLVING?

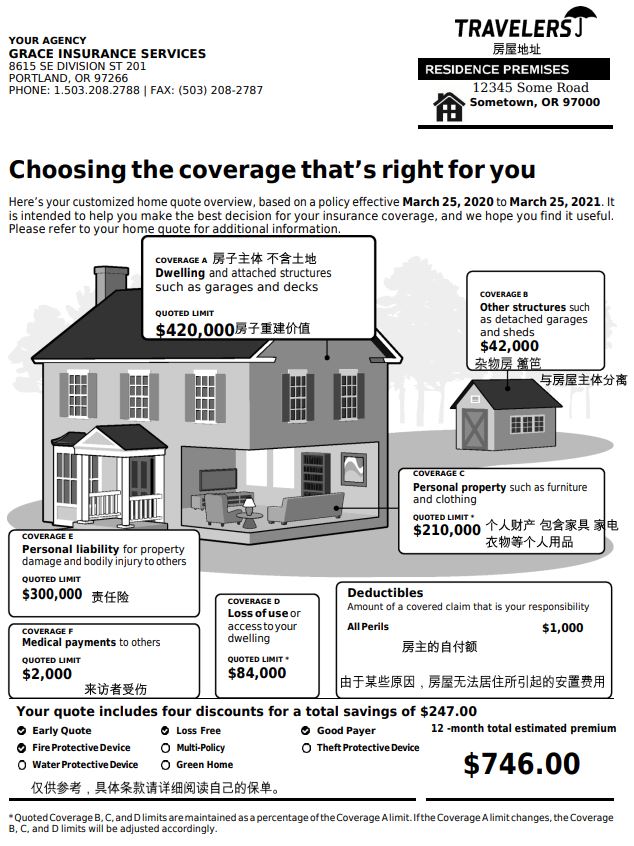

Choosing the coverage that is right for you.

Why did my rate change after I received a quote?

Several factors could influence why your rate changed between the time you received your quote and the time you decided to purchase your policy. If it's been a few months since you received your quote, it's possible we revised rates in your area, which could decrease or increase the price you pay for auto insurance. If you received a quote recently, it's possible something on your driving record - or the driving records of others on your policy - prompted a change in the quoted price.

Is my payment accepted immediately?

If you make a payment online, by phone or by mobile phone, we will accept your payment immediately. If you have automatic payments set up, your payment will be accepted on the regularly scheduled date. If you mail your payment, we will note the postmark date on your envelope and consider your payment to be made on that date.

How does progressive determine my insurance rate?

Progressive, like other insurers, groups customers based on similar characteristics, evaluates their claims experiences within these groups, and determines what to charge individuals with characteristics similar to members of the group. We charge a higher rate for customers more likely to have claims, and a lower rate for customers less likely to have claims.

Who is eligible for Health Insurance Marketplace?

To be eligible to use the Health Insurance Marketplace, you:

Get a quick Marketplace overview on the "A quick guide to the Health Insurance Marketplace" page to help you apply.

- Must live in the United States

- Must be a U.S. citizen or national (or be lawfully present)

- Can't be incarcerated.

Get a quick Marketplace overview on the "A quick guide to the Health Insurance Marketplace" page to help you apply.

Jewelry and cash coverage?

Step 1

Identify all valuable jewelry in your collection to insure. Inventory gold, platinum, pearls, diamonds, wedding or engagement rings, collectible costume jewelry, antique jewelry and watches. These items may be difficult or expensive to replace if lost or damaged; thus, having adequate insurance coverage is a necessity.

Step 2

Review existing policies to make sure you do not double-insure your items. If you have homeowners or renters insurance, check how much coverage is available for valuable jewelry. Note the situations covered: lost, stolen, destroyed or damaged. If you don't have a homeowners or renters policy, you may have to buy a stand-alone jewelry insurance policy.

Step 3

Get the jewelry appraised for insurance. Use the services of a professional appraiser or gemologist. Obtain a certificate of appraisal.

Step 4

Arrange an affordable deductible amount. Assess how much out-of-pocket expense you can afford in case of theft, loss or damage. Use this amount as your deductible.

Step 5

Check the type of insurance policy appropriate for the jewelry. Generally, insurance providers offer a "cash value" and a "replacement value" policy. Cash value pays the market value of lost or damaged jewelry. Replacement value policies pay replacement cost. Contact your homeowners/renters insurance companies to obtain and evaluate coverage and premiums. Also, contact jewelry insurance providers to include in your review. Most insurance companies provide online quotes.

Step 6

Schedule regular inspections for all insured valuable jewelry. Inspect your jewelry for maintenance and to secure stones and settings once or twice a year. During inspection, find out how much your jewelry is worth. Valuable and collectible jewelry may go up in value over time and this may require an adjustment to insurance policies.

Identify all valuable jewelry in your collection to insure. Inventory gold, platinum, pearls, diamonds, wedding or engagement rings, collectible costume jewelry, antique jewelry and watches. These items may be difficult or expensive to replace if lost or damaged; thus, having adequate insurance coverage is a necessity.

Step 2

Review existing policies to make sure you do not double-insure your items. If you have homeowners or renters insurance, check how much coverage is available for valuable jewelry. Note the situations covered: lost, stolen, destroyed or damaged. If you don't have a homeowners or renters policy, you may have to buy a stand-alone jewelry insurance policy.

Step 3

Get the jewelry appraised for insurance. Use the services of a professional appraiser or gemologist. Obtain a certificate of appraisal.

Step 4

Arrange an affordable deductible amount. Assess how much out-of-pocket expense you can afford in case of theft, loss or damage. Use this amount as your deductible.

Step 5

Check the type of insurance policy appropriate for the jewelry. Generally, insurance providers offer a "cash value" and a "replacement value" policy. Cash value pays the market value of lost or damaged jewelry. Replacement value policies pay replacement cost. Contact your homeowners/renters insurance companies to obtain and evaluate coverage and premiums. Also, contact jewelry insurance providers to include in your review. Most insurance companies provide online quotes.

Step 6

Schedule regular inspections for all insured valuable jewelry. Inspect your jewelry for maintenance and to secure stones and settings once or twice a year. During inspection, find out how much your jewelry is worth. Valuable and collectible jewelry may go up in value over time and this may require an adjustment to insurance policies.

What happens if I mail a payment on the due date?

We consider the postmark date on your envelope as your payment date, so even if you mail a payment on the due date, your payment will be considered on time.

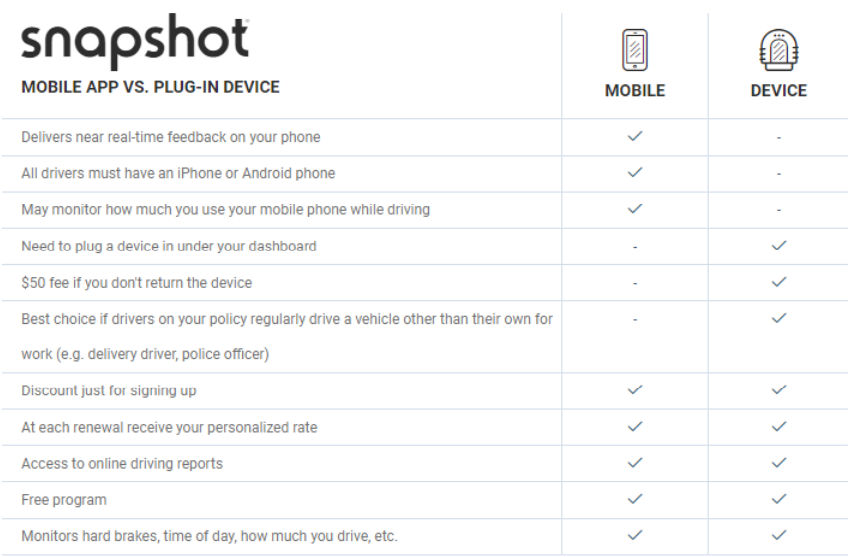

Snapshot rewards you for good driving with Progressive

Snapshot rewards you for good driving

Progressive's Snapshot program personalizes your car insurance rate based on your actual driving. It's technically called usage-based insurance. That means you pay based on how and how much you drive instead of just traditional factors. In most states, you get an automatic discount‡Read the associated disclosure for this claim. just for participating and a personalized rate at renewal depending on your results. While your rate could increase with high-risk driving, most drivers save with Snapshot. In fact, drivers who save with Snapshot save an average of $156 a year.*Read the associated disclosure for this claim.

Customer drives as they normally would

The customer can view driving reports and Snapshot performance on their phone and watch as they shape their rate. Hard brakes, harsh accelerations, late weekend drives, handheld phone usage, frequency and duration of trips are all monitored. The customer will receive a personalized rate at every renewal.

Progressive's Snapshot program personalizes your car insurance rate based on your actual driving. It's technically called usage-based insurance. That means you pay based on how and how much you drive instead of just traditional factors. In most states, you get an automatic discount‡Read the associated disclosure for this claim. just for participating and a personalized rate at renewal depending on your results. While your rate could increase with high-risk driving, most drivers save with Snapshot. In fact, drivers who save with Snapshot save an average of $156 a year.*Read the associated disclosure for this claim.

Customer drives as they normally would

The customer can view driving reports and Snapshot performance on their phone and watch as they shape their rate. Hard brakes, harsh accelerations, late weekend drives, handheld phone usage, frequency and duration of trips are all monitored. The customer will receive a personalized rate at every renewal.

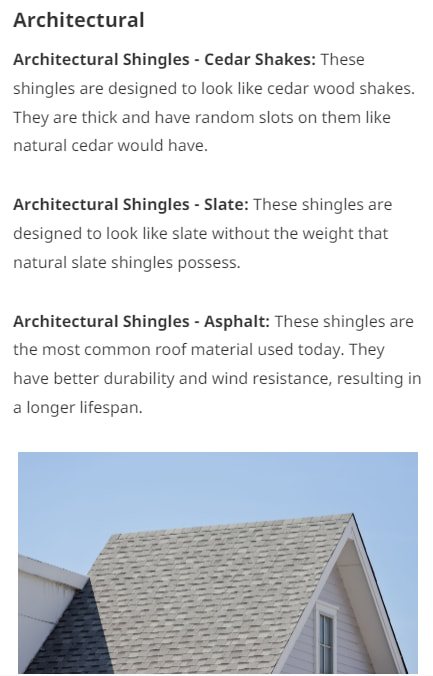

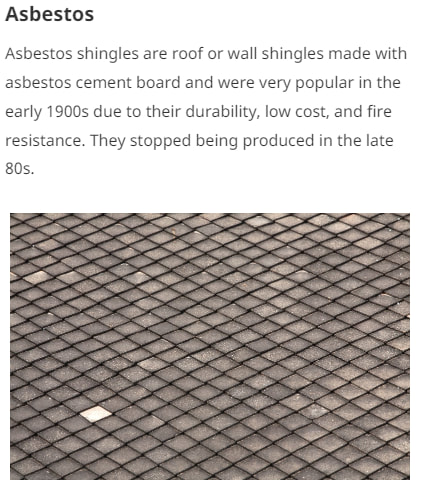

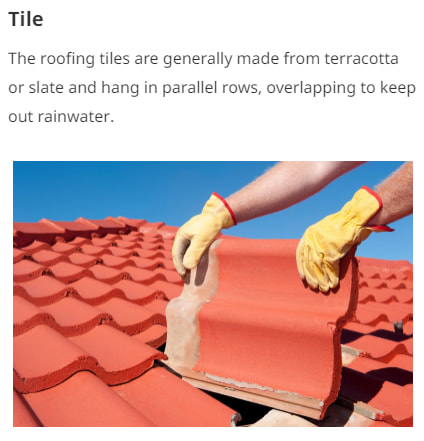

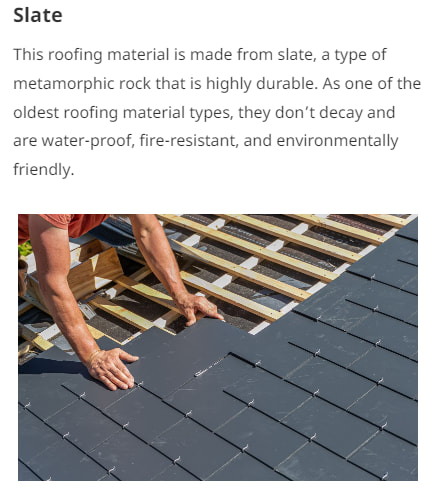

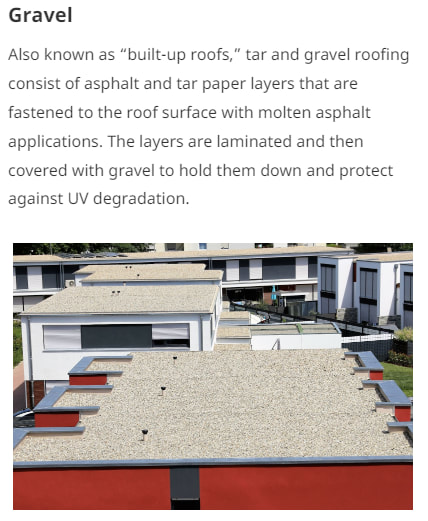

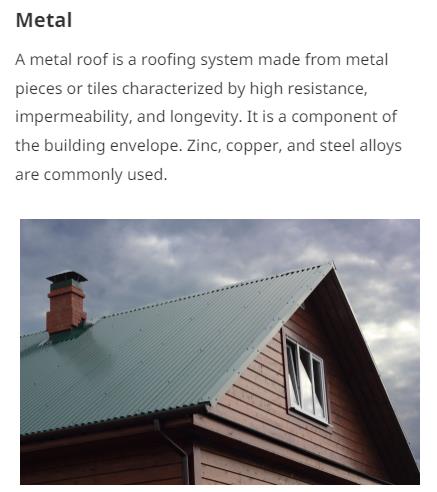

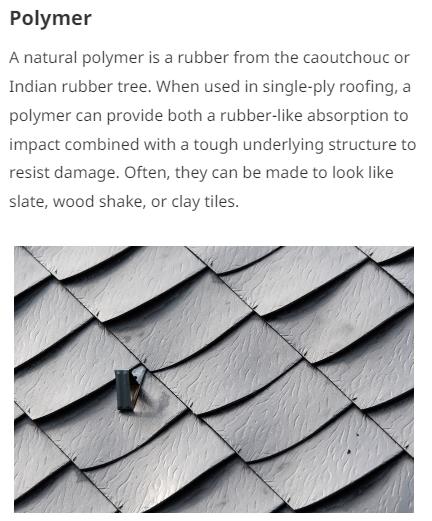

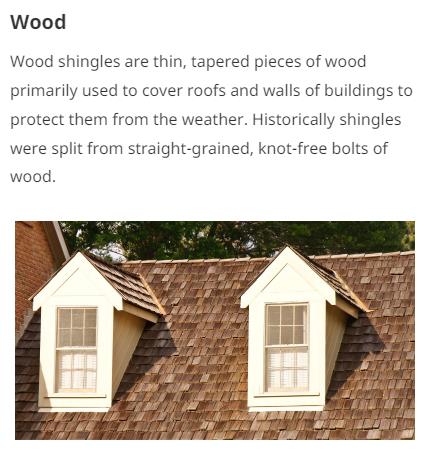

ROOFING MATERIALS REFERENCE

Why should I buy condo insurance?

Why should I buy condo insurance?

You may be thinking, “My condo association has insurance. Aren’t I already covered?” The answer: yes and no. While your condominium association insurance covers the building, you need a separate policy to protect your individual unit, personal property, and personal liability. That’s where ASI comes in, to fill in that gap for you and protect what your association’s master policy does not.

What does condo insurance cover?

The inside of your condo unit is likely filled with many personal belongings. Chances are, you also hold many of these items close to your heart, whether or not you live there full-time. If you own and occupy your condo unit for at least four months each year, a condominium units policy can cover:

With independent agencies across America, competitive rates and discounts, and the highest quality of experience for claims and customer service, ASI can help you obtain the right condominium insurance policy to fit your specific needs.

You may also be eligible for our Progressive Home program, which allows you to bundle your home and auto policy together. Call us 503-208-2788 to check the availability of Progressive Home for your condo insurance coverage.

source: americanstrategic.com/insurance/condo-insurance

You may be thinking, “My condo association has insurance. Aren’t I already covered?” The answer: yes and no. While your condominium association insurance covers the building, you need a separate policy to protect your individual unit, personal property, and personal liability. That’s where ASI comes in, to fill in that gap for you and protect what your association’s master policy does not.

What does condo insurance cover?

The inside of your condo unit is likely filled with many personal belongings. Chances are, you also hold many of these items close to your heart, whether or not you live there full-time. If you own and occupy your condo unit for at least four months each year, a condominium units policy can cover:

- Personal property within your unit

- Interior walls, fixtures, and other permanently attached building items inside your condo

- Personal liability and medical payments

With independent agencies across America, competitive rates and discounts, and the highest quality of experience for claims and customer service, ASI can help you obtain the right condominium insurance policy to fit your specific needs.

You may also be eligible for our Progressive Home program, which allows you to bundle your home and auto policy together. Call us 503-208-2788 to check the availability of Progressive Home for your condo insurance coverage.

source: americanstrategic.com/insurance/condo-insurance